Key points

– The surge in inflation should start to reverse next year.

– However, five structural trends suggest higher medium term inflation pressures than pre-pandemic. These are: a move away from economic rationalist policies; the reversal of globalisation; rising defence spending; climate change & decarbonisation; & a fall in workers versus consumers.

– This will likely constrain medium term investment returns compared to the pre pandemic years.

Introduction

It’s often said you don’t realise how good something is until it’s gone. This may apply to the low inflation environment that prevailed up to the pandemic. Apart from a few nasty interruptions this saw a downtrend in interest rates, mostly low unemployment, and an upwards trend in asset values (albeit it wasn’t so good for housing affordability). The explosion in inflation over the last year and the associated surge in interest rates and slump in investment markets makes it all seem like a distant memory.

The good news is that, as we noted in our last note (here), there is reason to believe the short term surge in inflation may be peaking (led by the US) & this, along with various other factors, may result in a better cyclical outlook for shares over the next 12 months. The bad news, as we have noted in various reports (see, eg, here), is that we have likely seen the bottom in the long-term decline in inflation from the early 1980s and inflation is likely to be higher over the medium term than pre-pandemic. This note takes a look at the five key structural factors driving this. (Two of these are a subset of global trends covered by my colleague (see here).)

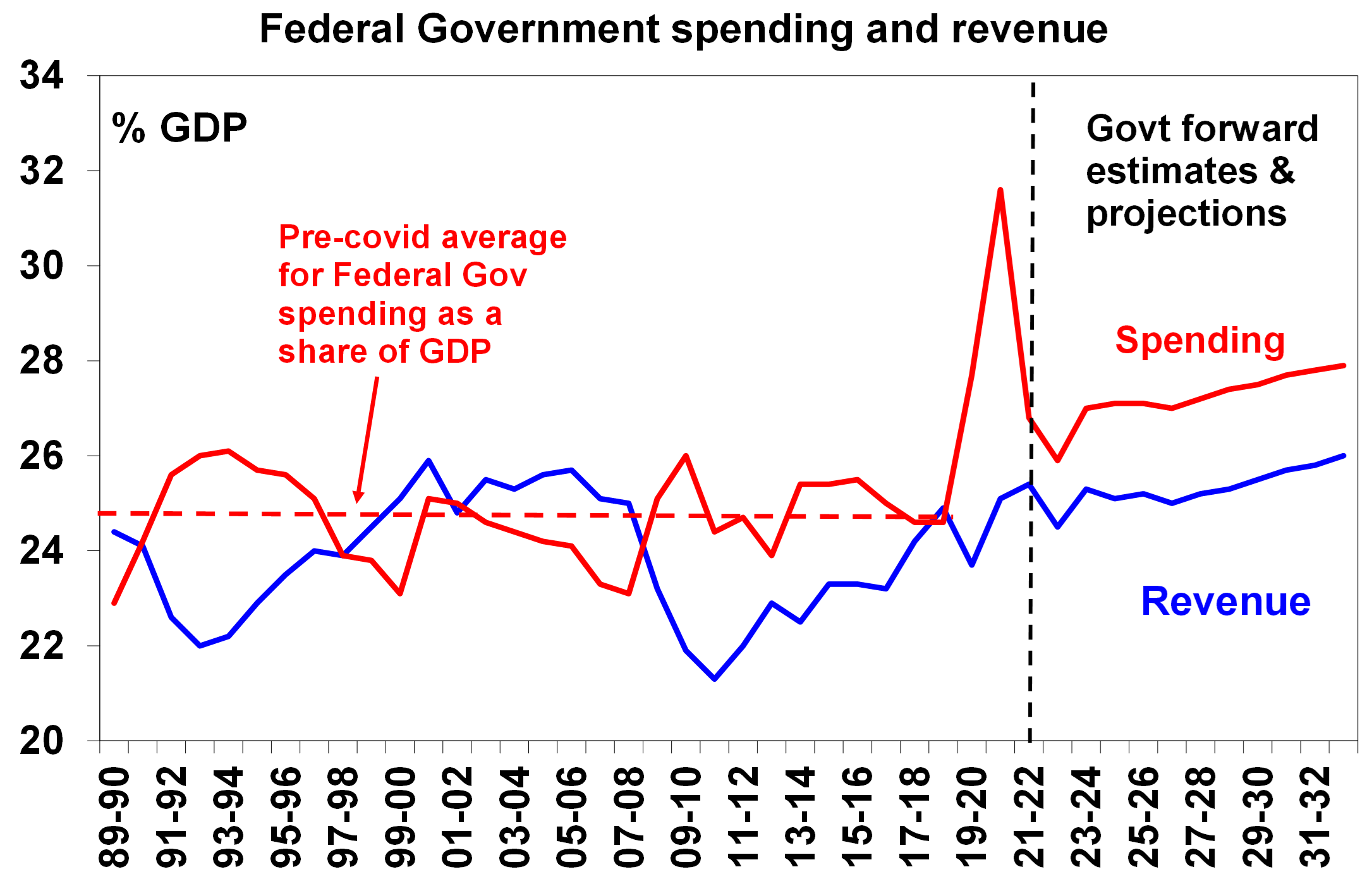

1. Bigger govt, less economic rationalist policies

The reaction to the inflationary malaise of the 1970s was the economic rationalist policies of Margaret Thatcher, Ronald Reagan and Bob Hawke and Paul Keating in Australia. These focussed on boosting the ability of the economy to supply goods and services by: limiting government involvement in the economy through policies such as deregulation and privatisation; policies to boost competition; measures to boost incentives by lowering tax rates; and labour market reform to make labour markets more flexible. This all helped lower inflation. Now as a result of the problems highlighted by the GFC, rising inequality, stagnant wages, aging populations, climate concerns and a collective memory loss regarding the lessons of the past there is a backlash against economic rationalist policies and more support for government intervention in the economy. It’s evident in Australia, for example, with the rising trend in government spending and revenue as a share of the economy, widespread pressure to raise taxes, together with measures to return to multi-industry bargaining within the labour market. The risk is that greater government involvement in the economy leads to lower productivity growth which will hamper the supply side of the economy and add to inflationary pressure.

Source: Australian Treasury, AMP

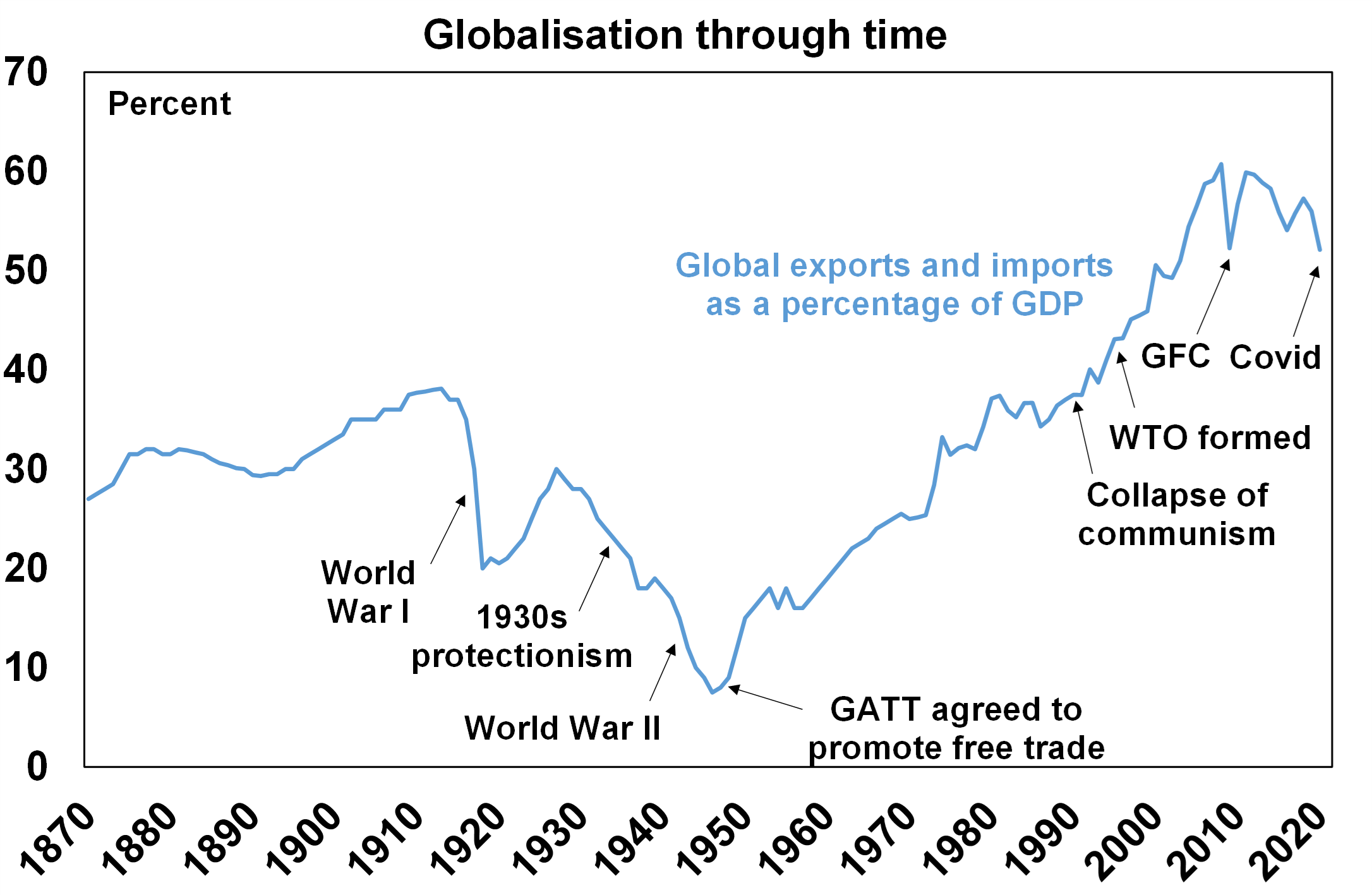

2. The reversal of globalisation

The post-World War Two period saw a huge surge in global trade and financial links between countries as more countries entered the global trading system and trade barriers collapsed. This saw a huge rise in global trade as a share of global GDP since the end of WW2 and the General Agreement on Tariffs and Trade (GATT). This was given a boost from the 1990s with the integration of China and Eastern block countries into global trade along with the formation of the World Trade Organization. This saw production allocated globally according to comparative advantage and the development of highly integrated global supply chains. The cost reductions and competition helped reduce inflation.

Source: World Bank, BCA, AMP

But the trend towards freer trade stalled in the 2000s, trade barriers are on the rise and trading blocks are being formed. The pandemic and rising geopolitical tensions are accelerating this reversal as countries seek to onshore production to reduce threats to supply chains spurred on by resurgent nationalist sentiment and a return to scepticism of free trade. The reversal of globalisation looks like it has a way to play out yet. Inevitably it will lead to higher costs and hence inflationary pressure.

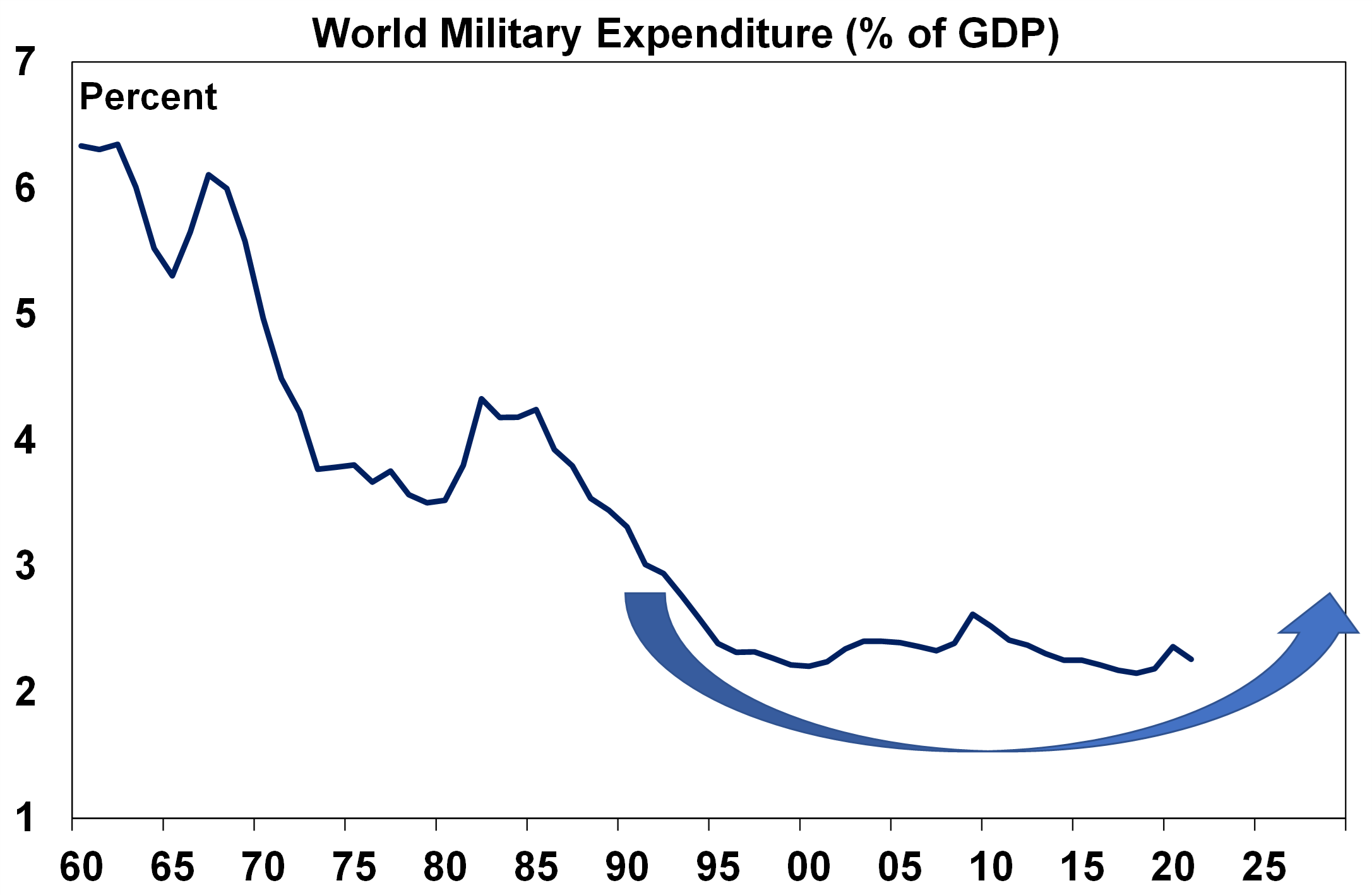

3. Increasing defence spending

Over much of the last 60 years world military spending as a share of global GDP has been in decline. The most recent fall started in the 1980s and got a push along by the ending of the Cold War. This took pressure off metal prices (as military spending tends to be metal intensive) and it helped keep government spending down, which freed up resources for use by the private sector. Both of which were disinflationary.

Source: World Bank, SIPRI, AMP

Now military spending is on the rise again, spurred on by the Russian invasion of Ukraine & China tensions. Even Germany & Japan are boosting military spending, as is Australia. This means more demand for metals and more government spending which will add to inflationary pressure

4. Climate change and decarbonisation

Ultimately the shift to sustainable energy could result in lower costs as energy from sources like wind and solar is cheaper than energy from most fossil fuels & still getting cheaper as the technology evolves. But we are a long way from that yet and climate change and the transition to net zero will likely add to costs & inflation in multiple ways via: increased extreme weather damage resulting in higher and more variable food and road transport costs; associated rebuilding costs & higher insurance premiums; costs associated with mitigation; increased demand for metals as economies retool for sustainability (eg an electric car uses 6 times more copper than a petrol car); increased energy costs as we are not seeing the usual supply enhancing investment response in fossil fuels to higher energy prices; and increased pollution regulation will add to costs like the anti-pollution equipment of the 1970s added to inflation at the time.

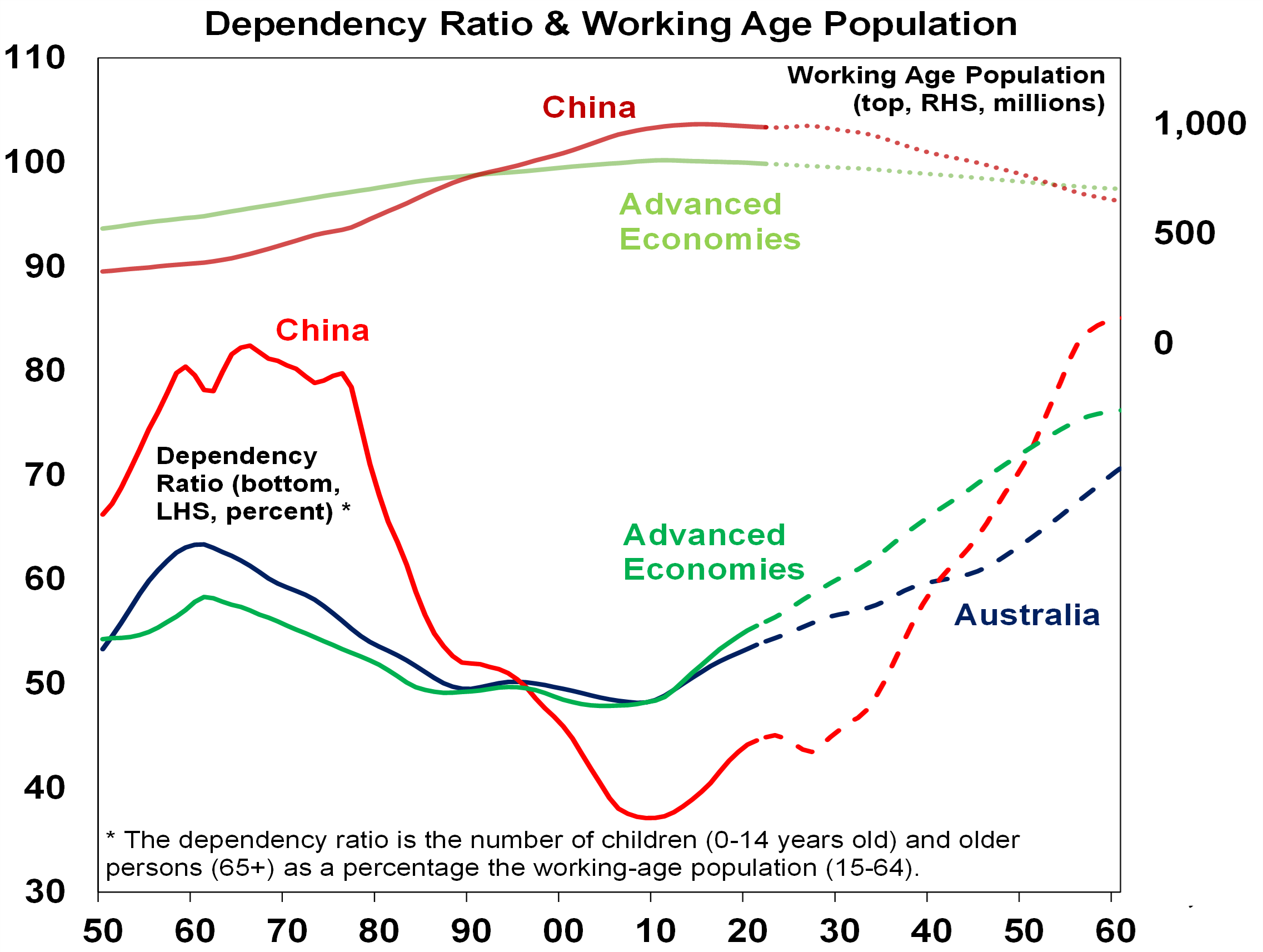

5. Less workers, more consumers

Demographic trends are changing in a number of key ways. Global population growth is slowing, while in advanced countries and China the working age population is now in the process of peaking and starting to decline (see the top portion of the next chart). And, as is well known, populations are aging, resulting in a rise in the ratio of children and older people to working aged people, ie the dependency ratio is rising (bottom portion of the next chart). Thanks to its high immigration program Australia is in a somewhat better position (with a still rising workforce and slower rising dependency ratio). But globally, the upshot is less workers (supply) & more consumers (demand) which will likely add to inflationary pressures. Similarly, “adverse for inflation” demographic trends are flowing from the entry to the workforce of inexperienced millennials and Gen Z as highly experienced baby boomers retire (which is bad for productivity) and the pandemic refocussing workers on quality-of-life making them more demanding in terms of pay and/or retiring early.

Source: UN, AMP

Implications for inflation

RBA Governor Lowe has referred to some of these structural forces as adding to inflation variability. But they are also likely to make economies more inflation prone as they imply more constrained supply & increased demand in some areas. For the technically minded this implies the supply curve shifting to the left and potentially being steeper and the demand curve (eg, for commodities) potentially shifting to the right. There is some offset with technological innovation still bearing down on prices, but the net effect will likely mean higher average inflation and possibly greater variability in it over time than pre-pandemic. The more inflation prone environment means central banks will have to work harder to keep inflation down around their 2-3% targets than pre-pandemic. Higher household debt levels in countries like Australia will aid in this as it makes monetary policy more potent than it was in the 1970s when household debt was low. It will probably still require higher & more variable interest rates than we saw pre-pandemic though.

Implications for investment returns

The collapse in inflation from the 1980s provided a tailwind for investment returns relative to what nominal growth and investment yields would normally indicate because it meant: lower interest rates; reduced economic volatility and uncertainty (and hence lower risk premiums); and a higher quality of company earnings. For growth assets it meant a valuation boost as shares traded on higher price to earnings multiples and real assets like property traded on lower income yields.

Higher inflation over the medium term than in the pre-pandemic period will remove this tailwind and threaten its reversal:

- Higher interest rates will make cash and fixed interest relatively more attractive to investors.

- Price to earnings ratios on shares will likely settle at lower levels and income yields on real assets at higher levels.

- Higher mortgage rates will mean a lower capacity to borrow and hence pay for homes meaning more constrained home prices.

If inflation averages around central bank targets, which is our base case, returns will be constrained but still reasonable. If alternatively, inflation turns out much higher then returns risk being weak. Which makes it very important central banks are successful in keeping inflation down – it’s just that the structural backdrop means it will likely be harder going forward.

![]()